How to File a Water Damage Insurance Claim in South Carolina

Step-by-step guide for Fort Mill & Rock Hill homeowners. What's covered, how to document damage, and how Carolina Pro Restoration handles the claims process for you.

Your basement just flooded. There's water coming through the ceiling. A pipe burst while you were at work.

The first thing most Fort Mill and Rock Hill homeowners ask after they get the damage under control is: "Is this covered — and what do I do now?"

This guide walks you through the claims process step by step, in plain language. No insurance jargon, no runaround. Just what to do and when to do it.

Does Your Homeowners Policy Cover This?

Before you do anything, you need to know whether your policy applies.

South Carolina homeowners insurance typically covers:

- Water heater failures

- Washing machine and dishwasher overflows

- Toilet supply line breaks

- Sudden roof leaks that let rain in

What it usually does NOT cover:

- Flooding from rivers, streams, or rising groundwater — that requires a separate flood insurance policy through FEMA's National Flood Insurance Program

- Slow leaks you knew about and didn't fix

- Gradual seepage through foundation walls

- Sewer backup (unless you added that endorsement to your policy)

- Neglected maintenance issues

The key word your insurance company will focus on is "sudden and accidental." If the damage happened fast and without warning — a pipe burst, an appliance failed, a storm knocked something loose — you are almost always covered. If the damage built up slowly over months, they may deny it.

If you're not sure which category your damage falls into, call us before you call your insurance company. We've handled hundreds of claims across York County and can tell you what you're likely looking at.

Step 1: Stop the Water First

Before you touch your phone, stop the source if you can.

- Appliance leak — pull the plug and shut off the water supply line behind it

- Roof leak — put a bucket down and don't go on the roof yourself

Then turn off electricity to any affected rooms if you can do so safely. Water and live outlets are a serious hazard.

Once the source is stopped, call Carolina Pro Restoration at 980-277-3700 . We dispatch crews 24 hours a day, 7 days a week. Getting water damage restoration started within the first hour makes a significant difference in how much you can save and how much your claim will cover.

Step 2: Document Everything Before Cleanup Starts

This is the step most homeowners skip — and it's the one that hurts them most later.

Take photos and video of everything before anything is moved or dried:

- Every room with visible damage

- The source of the water

- Wet floors, walls, and ceilings

- Damaged furniture, appliances, and personal items

Get down low and shoot at floor level. Capture the waterline on walls. If you have a second floor bathroom that leaked into a first floor ceiling, photograph both. The more documentation you have, the stronger your claim.

Also write down the time you discovered the damage and the first thing you noticed. Insurance companies ask for this detail and it matters.

Step 3: Call Your Insurance Company

South Carolina law does not set a hard deadline to file a claim, but you should notify your insurer as soon as possible — ideally within 24 to 48 hours of discovering the damage.

When you call, have these ready:

- Your policy number (on your declarations page or in your insurance app)

- The date and time you discovered the damage

- A brief description of what happened

- Your contact information and the property address

This first call is called the First Notice of Loss (FNOL) . You are simply reporting that a loss occurred and that you intend to file a claim. You do not need to have all the details sorted out at this point.

Your insurer will assign a claim number and an adjuster. Write both down.

Step 4: Let the Professionals Document the Damage

Once your insurance company is notified, a claims adjuster will be assigned to inspect your property. In South Carolina, your insurer is required to acknowledge your claim promptly after receiving notice.

Here's what most homeowners don't know: you don't have to wait for the adjuster before starting mitigation work. In fact, your policy likely requires you to take reasonable steps to prevent further damage right away. Waiting for an adjuster before extracting water could actually give your insurer grounds to reduce your payout if mold develops in the meantime.

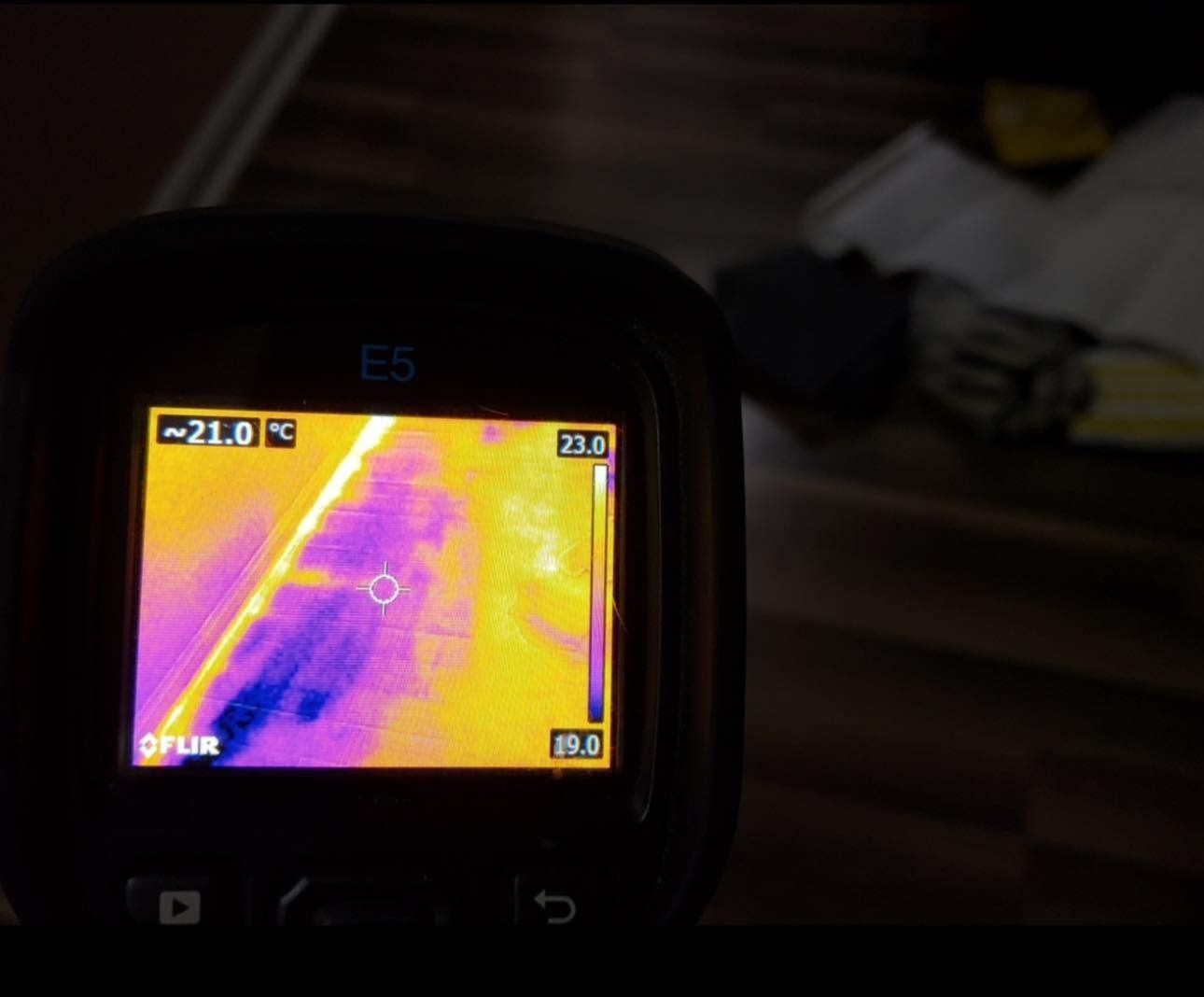

This is why calling a restoration company immediately matters. We document everything with:

- FLIR thermal imaging showing moisture behind walls and under floors

- Daily moisture meter readings at multiple points throughout the structure

- Dated photos of all affected areas

- A written scope of work in Xactimate — the same estimating software your adjuster uses

That Xactimate estimate is important. When your restoration company and your adjuster are working from the same software with the same local pricing data, your claim moves faster and there is less room for the insurance company to dispute line items.

Step 5: Understand Your Estimate and Adjuster's Offer

After the adjuster inspects your property, they will issue a scope of loss — a detailed breakdown of what they believe the repair will cost.

Review it carefully. A few things to watch for:

Actual Cash Value vs. Replacement Cost Value

Your policy is either an ACV policy or an RCV policy. ACV pays you the depreciated value of what was damaged. RCV pays you what it actually costs to replace it with something of like kind and quality. If your 10-year-old hardwood floors were destroyed, an ACV policy might pay a fraction of what new floors cost. An RCV policy pays for new floors.

Check your declarations page. It will say which type of coverage you have.

Depreciation Holdbacks

On RCV policies, insurers often issue an initial payment minus depreciation. You receive the depreciation portion after the repairs are completed and you submit proof. Don't spend that first check assuming it's the full amount — there may be more coming once the job is done.

If our Xactimate estimate and the adjuster's estimate don't match, we handle that conversation for you. We work directly with your adjuster to align on scope. You should never have to negotiate with your insurance company yourself.

Step 6: Get the Work Done and Close the Claim

Once the scope is agreed on, we move into the rebuild phase. This includes replacing drywall, painting, installing new flooring, fixing cabinetry, and finishing trim — whatever your home needs to get back to where it was before the damage.

A few things to know during this phase:

Your mortgage lender may be on the check. If you have a mortgage, your lender is technically a co-owner of the property and most insurers are required to include them on claim payments above a certain threshold. You will need to work with your lender to get the funds released for repairs. This is normal and we can help you navigate it.

Keep every receipt for emergency expenses. If you had to stay in a hotel, eat out, or rent storage while repairs happened, your policy may cover those Additional Living Expenses (ALE). Save every receipt and submit them to your adjuster regularly.

Get a final drying certificate before the rebuild starts. We issue a drying certificate documenting that all moisture readings have returned to acceptable levels. This protects you if any mold questions come up later and supports your insurance documentation.

What We Handle for You

Dealing with water damage is stressful enough without also managing an insurance claim on your own. Here is what Carolina Pro Restoration takes off your plate:

- Full moisture mapping and documentation from day one

- Xactimate estimate written in the same format your adjuster uses

- Direct communication with your adjuster on scope and line items

- Daily moisture logs and photos that support your claim

- Final drying certificate before the rebuild phase begins

- Complete rebuild so you deal with one company start to finish

We have worked with virtually every major insurance carrier that operates in York County, South Carolina. We know how they work and how to get your claim processed without unnecessary delays.

Frequently Asked Questions

Does homeowners insurance cover mold that resulted from water damage?

If the mold grew because of a covered water damage event — a burst pipe, an appliance failure — most policies will cover mold remediation as part of the claim. If the mold developed because of a slow leak you knew about, it may not be covered. Speed matters here: the faster you address water damage, the less likely mold becomes a dispute point in your claim.

What if my claim is denied?

First, ask for the denial in writing with the specific policy language they're relying on. Then call us — we can review the scope of damage and help you determine whether the denial is valid or worth disputing. South Carolina law requires insurers to act in good faith. Unreasonable denials can be challenged.

Will filing a claim raise my rates?

It depends on your insurer and your claims history. One claim in several years typically does not cause a large rate increase. If the damage is significant — tens of thousands of dollars — the cost of not filing almost always exceeds any rate adjustment. We provide a free written assessment so you can see the full scope before you decide.

Does flooding from Hurricane Helene-type storms count as flood damage or water damage?

This is one of the most common questions we get from Fort Mill and Rock Hill homeowners after heavy storms. If water entered your home because rain came through a damaged roof or a broken window — that is covered by your homeowners policy. If water entered from the ground up — rising streets, overflowing Sugar Creek, storm surge — that is flood damage and requires a separate NFIP flood insurance policy. We can help you figure out which category your damage falls into.

How long does the claims process take?

South Carolina law requires your insurer to pay an approved claim within 90 days of receiving your demand for payment. Most straightforward claims resolve much faster than that — often within 2 to 4 weeks. Complex claims involving sewage cleanup , crawlspace damage , or structural issues can take longer depending on scope.

Filing a water damage claim in South Carolina is not as complicated as it feels in the middle of a crisis. The keys are moving fast, documenting everything, and working with a restoration company that knows how to speak your adjuster's language.

If you've got water damage right now — or you're not sure whether what you're seeing qualifies — call us. We'll come out, assess the situation, and tell you exactly what you're dealing with at no charge.

Call Carolina Pro Restoration anytime at 980-277-3700 .

We serve Fort Mill, Rock Hill, Indian Land, Tega Cay, Charlotte, Pineville, Waxhaw, and the surrounding areas 24 hours a day, 7 days a week.

Carolina Pro Restoration LLC is a water damage restoration company serving Fort Mill SC, Rock Hill, Indian Land, Tega Cay, and the greater Charlotte area. We specialize in water damage restoration , mold remediation , crawlspace encapsulation , sewage cleanup , and full property rebuild. IICRC certified. Available 24/7. Direct insurance billing through Xactimate.

Official Carolina Pro Restoration Blog

Water Damage in Charlotte NC: What to Do in the First 24 Hours

Water Damage Restoration in Matthews NC: What Homeowners Need to Know

7 Signs You Have Hidden Water Damage in Your Fort Mill or Rock Hill Home

Dealing With Water Damage Right Now?

Our Fort Mill team answers 24/7 and can be on site fast. One call, one crew, start to finish.